UGREEN Tech's NAS Business Soars 213%, Net Profit Jumps 52%, But Why Is Its Stock Still Trapped in Volatility?

[Ebrun Exclusive] April 2 - Recently, UGREEN Tech (301606.SZ) released its full-year 2025 financial report, showcasing the company's robust growth momentum and profitability.

The company achieved annual operating revenue of 9.491 billion yuan, a year-on-year increase of 53.83%, marking a significant leap in revenue scale. Net profit attributable to shareholders reached 705 million yuan, up 52.42% year-on-year, while adjusted net profit was 680 million yuan, increasing by 53.97% year-on-year.

Despite the impressive performance, the secondary market's reaction has been erratic.

On the day of the earnings release, its stock price edged up 0.10%, plummeted 3.67% the next day, and then rebounded strongly by 5.05% the following day. Yesterday's closing price has recovered to levels seen before the major volatility in mid-March. In fact, over the past month, the stock has exhibited extremely high volatility, with its price swing approaching 40% of the current price.

Behind the stellar results, UGREEN finds itself caught in a tug-of-war between bulls and bears:

the remarkable rise of its NAS business has brought a valuation far exceeding that of its peers, but also puts its "heavy on marketing, light on R&D" operational strategy to the test in the new market dynamics.

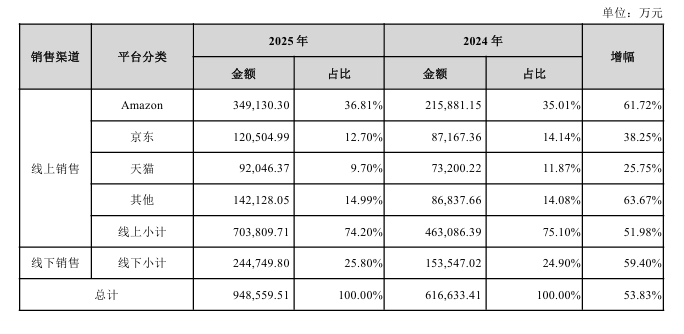

Cross-border business grew rapidly, offline channel expansion remained steady, and reliance on Amazon increased instead of decreasing.

In 2025, UGREEN continued to accelerate its growth in overseas markets.

Geographically, revenue from overseas markets reached 5.821 billion yuan, a year-on-year increase of 64.27%, accounting for 61.34% of total revenue and becoming the core growth driver. Domestic revenue was 3.664 billion yuan, up 39.71% year-on-year, indicating steady penetration in the home market.

Meanwhile, in terms of channel strategy, UGREEN demonstrated a trend of "strengthening strengths and diversifying points of growth."

Amazon remains the core revenue source, with its dominance continuing: during the reporting period, Amazon contributed 3.491 billion yuan in revenue for UGREEN Innovation, a 61.72% year-on-year increase, accounting for 36.81% of total revenue—a slight increase from the previous year.

Other cross-border channels (including independent websites, AliExpress, Lazada, Shopee, Noon, TikTok, etc.) collectively generated revenue of 1.421 billion yuan, a significant 63.67% year-on-year increase.

On domestic e-commerce platforms, UGREEN achieved revenues of 1.205 billion yuan on JD.com and 920 million yuan on Tmall, with growth rates of 38.25% and 25.75%, respectively.

Overall, online channels remain UGREEN's primary sales arena. In 2025, its online revenue totaled 7.038 billion yuan, accounting for 74.20% of total revenue, a 51.98% year-on-year increase. Offline revenue was 2.447 billion yuan, representing 25.80% of total revenue, surging 59.40% year-on-year.

Notably, UGREEN has shown ambition in "reshaping offline" channels.

During the reporting period, the company actively expanded its offline distribution network globally through strategic partnerships with large supermarkets, specialized channels, and leading regional distributors. Overseas, it has successfully entered the distribution systems of major retail giants such as Walmart, Costco, Best Buy, B&H, and MicroCenter in the US; Media Markt in Europe; and Bic Camera and Yodobashi Camera in Japan.

NAS business stands out, "low-end disruption" strategy sweeps the globe, but its ceiling remains uncertain.

In 2025, UGREEN's traditional product lines performed steadily.

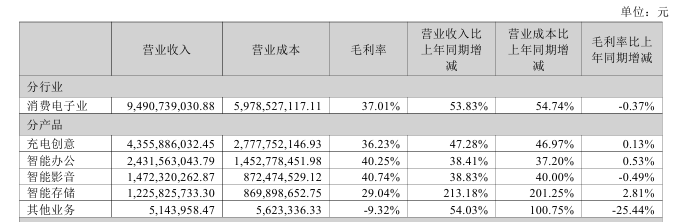

By category, revenue from Charging Innovations, Smart Office, and Smart Audio-Visual segments were 4.356 billion yuan, 2.432 billion yuan, and 1.472 billion yuan, respectively, increasing by 47.28%, 38.41%, and 38.83% year-on-year, accounting for 45.90%, 25.62%, and 15.51% of total revenue.

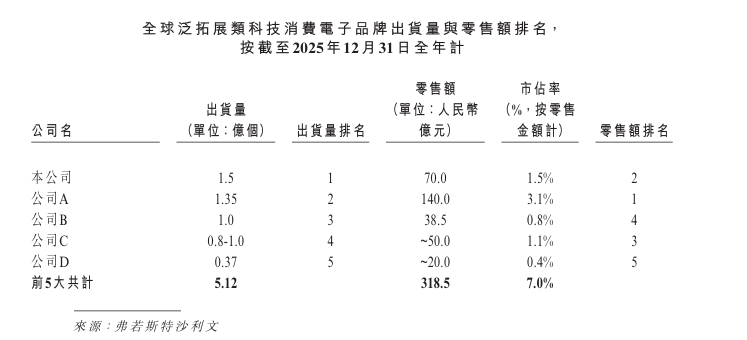

Within its core business, often categorized as "broadly expanding tech consumer electronics"—including charging products, audio-video products, connectivity/transmission products, and storage products—UGREEN secured another victory: according to Frost & Sullivan data, in 2025, UGREEN became the global leader in shipment volume for this sector.

However, the truly eye-catching performance came from its consumer-grade NAS business, which surged over the past year, partly driven by AI concepts like "OpenClaw".

It is reported that UGREEN began R&D on NAS-related technologies as early as 2018. 2020 marked the first year of commercialization for its NAS business, with the launch of its first private cloud storage product, the UGREEN Private Cloud DH1000.

Targeting "novice users" and "family sharing," the product significantly lowered the technical barrier of traditional NAS devices with its simple installation process and mobile app control, quickly gaining traction in the consumer electronics market.

In subsequent years, UGREEN launched several popular models, gradually progressing from entry-level "2-bay" devices to more powerful "4-bay," "6-bay," and "8-bay" models.

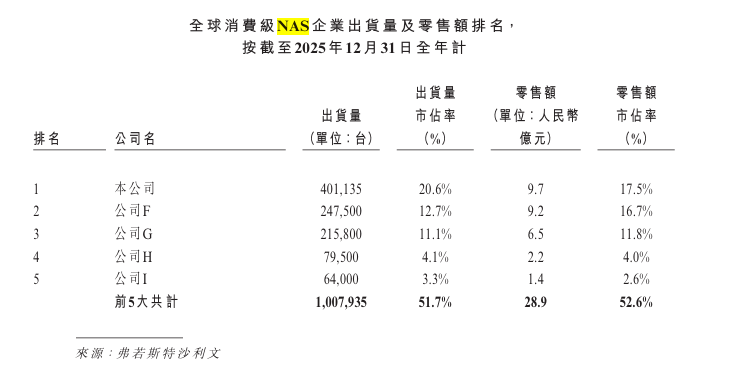

During the reporting period, revenue from the Smart Storage business (where NAS products reside) reached 1.226 billion yuan, skyrocketing 213.18% year-on-year, contributing 12.92% of total revenue and becoming a new growth engine.

According to data from its latest Hong Kong exchange prospectus, in 2025, UGREEN surpassed a host of established players and new entrants (inferred: Company F being Synology, Company G being QNAP, Company H being Buffalo, Company I being ZhiTi/ZSpace) in the consumer-grade NAS segment, taking a commanding lead to win the "double championship" in both shipment volume and retail sales.

UGREEN's ability to become a latecomer-turned-leader is closely tied to its unique product definition and market competition strategy. Fundamentally, UGREEN does not approach product development with the logic of "traditional IT equipment" but rather adheres to a "consumer electronics" logic:

it aims to transform private NAS from "servers only programmers can handle" into devices that are "as easy to use as a large USB drive—simple operation, smooth performance, intuitive interface." Its core focus is "out-of-the-box usability," eliminating the configuration and debugging required by traditional competitors.

Specifically, its competitive advantage lies in addressing the entry-level and mid-range needs of non-professional users, especially in scenarios like home entertainment, media creation, and high-speed data transfer. Targeting this customer base, its product strategy follows two main principles.

First, streamline redundant options, enhance commonly used functions, and emphasize the "smooth experience" of daily use.

Compared to deep system capabilities, complex architectures, and advanced features like Docker and virtual machines, UGREEN focuses more on aspects like HDMI output, video transcoding acceleration, and network throughput efficiency, ensuring that "ordinary users have a great experience" tailored to home entertainment, personal backup, and light content creation scenarios.

Second, "more features without a price increase," prioritizing hardware.

Within the same bay count and price segment, UGREEN often provides better hardware specifications (multi-core CPUs, larger memory, faster transfer speeds, etc.) than established brands at similar or even slightly lower prices.

This is akin to a "winning by clever strategy" approach: as a supply-chain-backed latecomer compared to players like Synology and QNAP, which have deep software and ecosystem expertise, UGREEN's tactic of competing on "specs and performance" allows it to quickly capture the entry-level market and avoid direct confrontation in areas where it is weaker. This is undoubtedly a clever strategy.

However, as the market potential becomes apparent, more competitors are emerging on this path. Whether UGREEN's moat is deep enough remains to be seen.

Ecosystem giants like Huawei, Xiaomi, and Lenovo have accelerated their entry in recent years. Leveraging their inherent ecosystem stickiness and massive user traffic, these giants can easily exert overwhelming pressure on independent manufacturers within their "walled gardens." Defending market share under the dual pressures of price wars and ecosystem bundling is no easy task.

Meanwhile, established overseas players like Synology, Western Digital, and Buffalo have also begun targeting the entry-level market with aggressive moves. A look at Amazon reveals that some of their mid-to-low-end SKUs are quite price-competitive, attempting to reclaim lost ground.

Furthermore, UGREEN's strategy of "emphasizing hardware and prioritizing scale expansion" puts pressure on its cost structure. The NAS business, which the market is most optimistic about, actually has a gross margin (28.1%) significantly lower than the company's other product lines. As a durable consumer good with a relatively long replacement cycle, it remains highly uncertain when the NAS business's profitability can recover to the company's average level.

Growth Concerns: High P/E Ratio, Low R&D Investment, Major Shareholder Cash-Outs, Tight Operating Cash Flow

After its rapid advance, whether UGREEN's market valuation is sufficiently reasonable and robust has become a focal point of capital market debate. Within the consumer electronics sector, compared to peers like Anker Innovations (P/E 22.62), Edifier (P/E 23.33), and Transsion Holdings (P/E 24.32), UGREEN's P/E ratio (40.78) appears exceptionally high.

However, stripping away the hype bubble from AI concepts, structural concerns underlying UGREEN's growth curve remain unresolved.

First, insufficient R&D intensity. Compared to a peer like Anker Innovations in similar fields, UGREEN's R&D investment is relatively small, amounting to only 437 million yuan last year, possibly less than one-fifth of Anker's. From the perspective of R&D expense ratio, UGREEN's data (4.61%) also lags behind Anker Innovations (8.60%) and Edifier (6.91%), only slightly higher than Transsion Holdings (3.67%), which has a much larger revenue base.

Meanwhile, among various costs, the growth rate of sales and marketing expenses has outpaced revenue growth. The issue of relying on marketing to drive growth persists.

However, the financial report shows that due to the expansion of its R&D team, R&D expenses surged 43.96% year-on-year last year, indicating a corrective signal towards reversing the "light on R&D" tendency.

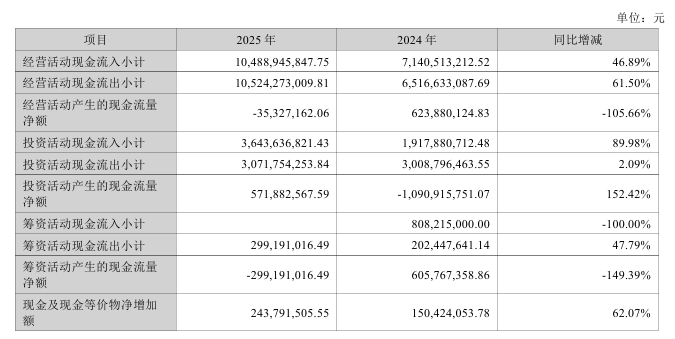

Second, operating cash flow turned negative.

In 2025, UGREEN's "net cash flow from operating activities" plummeted 105.66% year-on-year, turning negative. This indicates that although the company reported profits, it failed to generate actual cash from its core operations. The report attributed the sharp decline to increased cash payments for purchasing goods and other daily operating activities.

Meanwhile, the reason its net increase in cash and cash equivalents remained positive was partly due to contributions from investing activities: in 2025, "net cash flow from investing activities" was 572 million yuan, compared to -1.09 billion yuan the previous year, a surge of 152.42%.

Third, major shareholders and key executives cashed out nearly 1 billion yuan.

In late January 2025, UGREEN Tech faced its first major wave of lock-up share expirations. Subsequently, in February-March, its largest external shareholder, Hillhouse Capital (via Zhuhai Xiheng), cashed out approximately 509 million yuan. Vice President in charge of R&D Chen Yan and several other key executives (via platforms like UGREEN Management) cashed out approximately 472 million yuan.

These consecutive high-level share reductions have raised market doubts about the company's future prospects and likely contributed to the stock's decline following the earnings report.

In summary, 2025 was a year where UGREEN Tech delivered an excellent report card, establishing itself as a dark horse in the cross-border e-commerce race. Whether it can sustain this growth momentum and continue to capitalize on its successes in the future depends on its ability to transition from "catching trends" to "building high walls and storing ample provisions" (fortifying its competitive position).

Ebrun will continue tracking developments related to this story. To learn more information related to this article, please scan the QR code to follow the author on WeChat.

[Copyright Notice] Ebrun advocates respecting and protecting intellectual property rights. Without permission, no one is allowed to copy, reproduce, or use the content of this website in any other way. If any copyright issues are found in the articles on this website, please provide copyright questions, identification, proof of copyright, contact information, etc. and send an email to run@ebrun.com. We will communicate and handle it in a timely manner.

Translated by AI. Feedback: run@ebrun.com