Has the Golden Age Ended? Why Is Cross-Border Parcel Shipping Quietly Rebounding?

By Wang Yu Edited by He Yang

[Ebrun Original] On the fourth day of the Lunar New Year, close to midnight. The excitement in the cross-border merchant groups—exchanging red envelopes and wishes of "Gong Xi Fa Cai"—had faded. Suddenly, a message popped up: "Has the U.S. tariff been canceled?" followed by an English link: "Supreme Court Rules Trump Tariffs Illegal." This sparked a wave of discussion, and the group chat quickly scrolled. A seemingly casual question triggered a heated debate: If Trump's tariffs are illegal, could the accompanying cancellation of T86 (the simplified customs clearance mode under the de minimis rule for parcels under $800, officially canceled on May 2, 2025) possibly be revived? Over the past year, U.S. policies such as tariff hikes, cancellation of small-value duty exemptions, and enhanced customs scrutiny have caused significant turbulence for the direct parcel shipping model in cross-border logistics, once lamented as having "completed its historical mission." But if the T86 channel were restored—even just loosened—many merchants' cost structures, fulfillment rhythms, and operational strategies could be reshaped. The excitement didn't last half a day. The White House issued an executive order: imposing an additional 10% tariff on global imports (later, Trump claimed on social media to raise it to 15%), with the T86 channel remaining closed. The document stated: "The President believes that suspending the de minimis treatment remains necessary and appropriate." "Got our hopes up for nothing," someone remarked, and the group fell silent again. However, experienced merchants were not unsettled by this misjudgment. Even after last year's "tariff war," they had not entirely abandoned the parcel model but adjusted product selection and recalculated profit models. "Under the new policy environment, direct parcel shipping still generates profits, and order volumes remain manageable," one seller summarized. Several logistics service providers also revealed to Ebrun that parcel shipping volumes had quietly rebounded in the past six months. "Many peers resumed direct shipping product quotes early, and some of our long-term clients saw direct order volumes recover quickly (after T86 was canceled last year), even reaching new highs," a freight forwarder manager said. Deprived of policy benefits and without institutional rollbacks, direct parcel shipping is not "out of the game." What changes and constants lie behind its recovery?

01 After the Turmoil, the Golden Age of Cross-Border Parcels Is Over

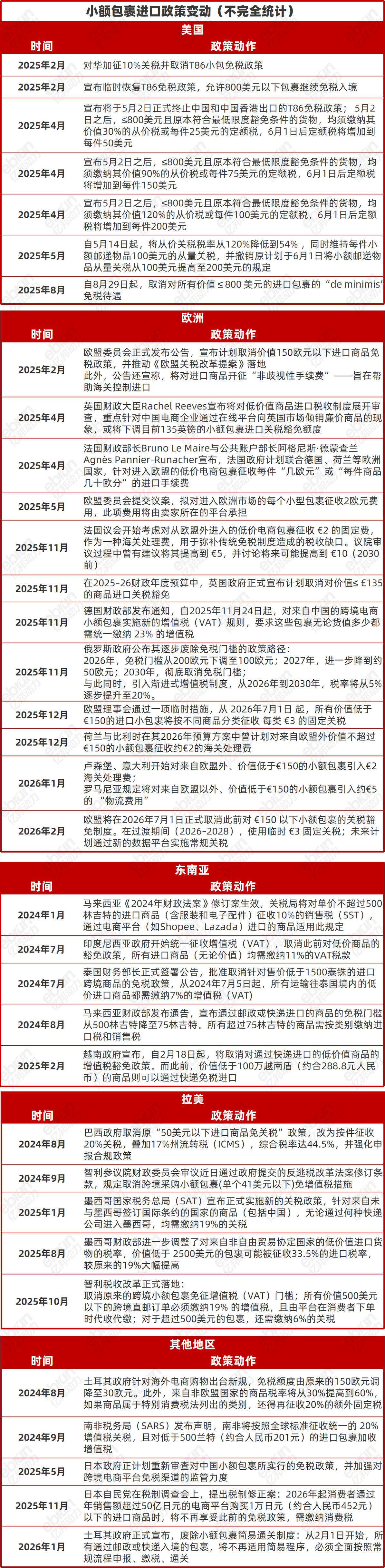

"The direct parcel shipping model has attracted the most firepower and endured the hardest hits over the past year," said Claire, an independent site seller highly reliant on this model. Aside from the U.S., almost no major market has refrained from "imposing restrictions or cutting benefits" on small-value import parcel duty exemptions. This is no exaggeration. In 2025, the guillotine for "small parcels" has fallen across major global markets.

However, the depth of the cut varies. EU countries adopted a strategy of "handling fees + fixed small tariffs"; Chile, Malaysia, Thailand, etc., prioritized closing gaps in collecting "non-tariff" taxes like VAT and sales tax. The pace of implementation also differed. For instance, the EU took nearly two and a half years from proposal to final signing; Turkey and Russia chose a gradual approach, slowly lowering duty-free thresholds and adjusting rates until eliminating parcel benefits entirely; earlier, India treated combating Chinese parcels as a political achievement, shutting down the de minimis channel within months. Among these, the U.S. is the most extreme case. The T86 policy underwent cancellation, temporary restoration, phased punitive rate hikes, adjustments, and final abolition within six months. Policy swings were unprecedented: in just two weeks in April 2025, parcel rates skyrocketed to 120% before dropping to 54%. Regions once seen as "safe harbors"—like Southeast Asia and Latin America—are now also "closing gaps." Developed economies emphasize "combating counterfeits and improving product safety," while emerging markets focus more on "protecting local industries and stabilizing tax bases." Without exception, both aim to prevent cross-border e-commerce players from operating outside regulatory oversight. This is not targeted action by any single country but a restructuring of global customs governance logic. The benefits of cross-border e-commerce parcels no longer offer "geographical substitutability"—losses in the West cannot be compensated by gains in the East. The new normal is the evaporation of gray areas and full integration into conventional import systems.

02 Bottoming Out and Rebounding? A Quiet Recovery?

Perhaps surprisingly, even without benefits, the direct parcel shipping model has not remained in a slump. Data from YunExpress, a leader in direct parcel shipping, showed that during last year's Black Friday/Cyber Monday period, its daily order volume increased 30% year-on-year, hitting a record high. Moreover, in this "turbulent" year, many overseas sellers joined its direct parcel network. Another top player, SFC Express, provided corroborating data. "Full-year 2025 was basically flat with 2024, with a slight increase of about 3%, indicating steady progress," revealed Fang Jie, its head of marketing. Currently, Amazon sellers account for about 70% of its client structure, while independent site and other platform sellers make up about 30%. By regional revenue share, Europe accounts for about 33%, the U.S. about 20%, Latin America about 20%, and Japan about 8%, with the U.S. and Japan seeing the most significant growth last year—order volumes nearly doubled.

Another major cross-border logistics provider, Jiu Fang Tong Xun, also noted that by the end of last year, its parcel business order volume had surpassed the previous year's level. Group Vice President Vigoss said the direct parcel segment still accounts for about 15% of overall revenue, with good growth momentum. "(The most severe impact was probably in May last year," Vigoss recalled. "Rates fluctuated wildly, swinging dozens of percentage points within half a month. Many sellers adopted a wait-and-see approach, and parcel orders dropped significantly. But the negative effects were mainly concentrated in those one or two months. After the turbulence, performance actually reached new highs." SFC Express also experienced a "bimodal curve" in 2025: a small surge of "panic stocking" at the end of May, followed by a slow, steady growth throughout the second half. "Even with tariff increases, overseas consumer demand for direct parcel shipped goods remains strong," Fang Jie said. On the other hand, after several rounds of shocks, many small and medium-sized freight forwarders have exited the industry or been forced to transform. "The early U.S. parcel market had many participants with varying service models and operational capabilities. But as the policy environment normalized, providers with stable operations and long-term investments in infrastructure and compliance systems demonstrated stronger overall risk resilience," Fang Jie explained. It can be said that the "policy earthquake" did not impact mainstream providers and their core clients as severely as initially feared—steady growth remains the main theme. "For the brand-oriented independent site sellers we serve, order volumes grew at least 50% to 100%, or even more, compared to 2024. Smaller sellers who hadn't scaled up previously are indeed having a hard time—those who used to get 1,000-2,000 orders a day might now see only 100-200 orders," Vigoss said, noting that the policy shock accelerated the polarization among merchants. "For us, in terms of revenue growth, the fluctuations have been largely smoothed out and absorbed." Ms. Forest Zhang, founder of Big Forest Logistics, pointed out that the main impact of the tariff turmoil was actually significant changes in work methods. With each tariff adjustment, rates, additional fees, etc., change, backend systems must sync with customs systems—quotes for clients must be promptly revised, involving not just cost figures but frequent adjustments to effective/expiration dates. "Such frequent changes are unprecedented, and the workload has indeed increased considerably," she said.

03 Who Is Still "Holding the Fort"?

"Based on our observations, merchants still using direct parcel shipping can be broadly divided into two categories based on their supply chain structure," stated SFC Express. The first category uses "overseas warehouse + parcel" in parallel—warehouse stocking primary, direct shipping secondary, with shipping volume ratios around 60/40 or 70/30.

"The overseas warehouse model has low tolerance for product selection errors; if items become stagnant, inventory costs can devour all profits. Parcels handle testing and filling gaps. This parallel model effectively hedges risks," Fang Jie explained. The second category is "100% direct parcel shipping," mainly traditional assortment-based sellers—with large, deep SKU counts and significant long-tail demand, unsuitable for overseas warehousing. Tariff hikes haven't "driven away" all assortment-based sellers. "Many self-media outlets readily tout narratives like 'the parcel model is dead, low-price assortment is finished'—it's overly alarmist," an Amazon seller told Ebrun. The actual impact of abolishing the small parcel duty exemption on assortment-based sellers boils down to precise cost-side actuarial calculations. Vigoss analyzed that for such sellers, procurement costs from sources like 1688 or factories are often just a few RMB. Even declaring at current tariff rates, the tax burden itself isn't high. Even including brokerage fees, merchandise processing fees, and other charges, following full compliance, the cost increase per parcel averages only about 2-3 RMB. "Compared to the final selling price, this cost increase is almost negligible. Sellers can easily absorb it through slight price hikes or even maintain original prices—sales volume won't be significantly affected," he said. Another contrasting phenomenon is emerging—some medium-to-large item sellers in categories like furniture are turning to direct shipping. "From our business data, the fastest-growing and best-selling segment now is actually medium-to-large item services," SFC Express noted, "especially sea freight direct large parcels, which can handle larger-sized packages with high cost-effectiveness, appealing to price-sensitive clients." This change breaks the stereotype that direct shipping only suits small, light items. Against the backdrop of intense competition in small, light items, many sellers have hit growth bottlenecks and are shifting to higher average order value, less homogenized categories with certain barriers, like furniture, fitness equipment, and tool racks. At its root, the resilience of the direct parcel model lies not in its shipping price advantage but more in fast turnover and low inventory. "Stagnant inventory loses big money; rising per-shipment costs lose small money. It's not hard to tell which is more important," said Lewis, a Temu seller, noting that direct parcel shipping is essentially a model with lower cost pressure and more stable cash flow. "For example, selling on SHEIN, many sellers have stocking cycles under 14 days, some compressible to 7 days, and some even achieve near real-time response—procuring or placing factory orders only after receiving orders. For them, it's basically zero deficit on the books," he said.

04 Logistics Providers Recalculate Costs

Control costs, is not only a cornerstone for merchants but also an essential "basic skill" for service providers. From a provider's perspective, a direct parcel's cost structure can be divided into four parts: 1) Pickup cost, largely unaffected by overseas market factors; 2) Linehaul cost, including allocation, air freight, export customs clearance, etc.; 3) Overseas customs clearance and tax costs; 4) Last-mile delivery cost. They need to find stable profit points amidst fluctuations in these four cost components. Fortunately, it's not as difficult as imagined. Taking the U.S. market as an example, the rise in "customs/tax" costs is the most obvious. "Calculations show that after T86 abolition, the cost increase for U.S.-bound parcels in customs clearance is about 10%-25%," a freight forwarder professional told Ebrun. However, this is offset by decreases in linehaul and last-mile costs. "On one hand, average air freight market prices declined overall last year, dropping about 3-5 RMB per kilogram; on the other hand, with new capacity supply, last-mile costs have also been significantly optimized," stated Jiu Fang Tong Xun. In recent years, more commercial delivery options have emerged in the U.S. market. Gofo, UniUni, SpeedX, etc., with Chinese capital backgrounds, expanded rapidly; meanwhile, domestic leaders like Yanwen and YunExpress also increased their last-mile layout in the U.S. Previously, providers relied on mainstream carriers like USPS, Pitney Bowes, ACI Logistix for "economy lines." But in the past year, several old players were eliminated, and new-generation commercial carriers quickly filled the gap, significantly reducing last-mile costs. "Take USPS: ounce-based items start around $3.5, pound-based items cost $5-7 per pound; commercial carriers can do just over $2, even with near-flat rates up to 10 pounds," Vigoss said. "Last-mile logistics cost savings per order can be several dollars—the cost difference is very significant; especially in higher weight brackets, the price difference can be three to five times." This cost advantage is closely tied to the "cherry-picking" strategy of Chinese-backed commercial carriers—they often focus intensely on core areas and mainstream service types, abandoning marginal businesses, thus outperforming traditional carriers with rigid models, full coverage, and poor flexibility in timeliness, loading efficiency, and cost control.

05 Expanding Revenue and Reducing Costs: Finding New Growth Levers

Beyond passively waiting for capacity price drops, many providers are actively "expanding revenue and reducing costs." In cost reduction, besides conventional methods like long-term agreements with customs brokers, last-mile carriers, and airlines to enhance bargaining power through scale, many providers are streamlining domestic pickup points through route planning: closing low-volume sites and adopting consolidation models to gather dispersed shipments at efficient nodes, thereby reducing costs. "Shedding burdens, shrinking frontlines, outsourcing instead of self-operating, purchasing third-party services—these are necessary moves for many mid-to-lower-tier providers lacking strength," a freight forwarder owner said. "Is full self-operation and vertical integration good? Of course! But when business volume hasn't reached economies of scale, facing so many black swan events, you have to sacrifice pawns to save the king, focusing resources on cash-flow-generating businesses." However, some large-volume logistics players are doing the opposite. To cope with cost pressures, Big Forest Logistics increasingly adopted self-operation for many overseas projects instead of outsourcing. For example, in delivery services and drayage, they increasingly use self-operated methods, planning routes and streamlining costs themselves. Meanwhile, in 2025, the company's overall strategy shifted from scale-oriented to profit-prioritized.

Jiu Fang Tong Xun initiated an organizational restructuring in 2025, deeply integrating its air freight and parcel departments from four major divisions, integrating key processes like shared linehaul capacity, front-end allocation, warehouse consolidation, and merged customs clearance. Combining capacity and human resources achieved a "1+1>2" effect: post-adjustment, both departments saw over 50%-60% revenue growth, while team size was slightly streamlined, significantly improving per-capita efficiency. In revenue expansion, different companies found different leverage points. According to Ebrun research, small and medium-sized forwarders often prefer "subtraction"—boosting popular products and cutting unpopular ones; while some established providers lean towards "addition"—seeking growth through comprehensive service coverage and refined services. SFC Express took the latter path. In the U.S. market, it achieved full product line coverage, including air freight small, medium, and large parcels, plus sea freight direct shipping. Relying on this product diversity—"whatever you sell, there's a channel"—the company maintained growth despite overall industry contraction. Additionally, another key product SFC Express recently promoted is "crowdfunding fulfillment." "We have deep experience in fulfilling overseas crowdfunding products. Starting this year, we are systematically packaging these experiences and capabilities to serve more sellers with related needs. Market feedback has been generally positive," Fang Jie introduced. Crowdfunding product fulfillment differs from regular e-commerce shipments in aspects like higher assembly difficulty, personalized packaging, and prioritizing overall fulfillment experience over pure speed. "It's like a 'Deluxe Plus upgrade' built on the traditional direct shipping model—a truly fully customized logistics product," Fang Jie said. "How to unearth innovative value-added services from traditional parcel shipping has been a key focus of our exploration in recent years."

Ebrun continues to track this intelligence. To learn more related information, please scan the QR code to follow the author on WeChat.

[Copyright Notice] Ebrun advocates respecting and protecting intellectual property rights. Without permission, no one is allowed to copy, reproduce, or use the content of this website in any other way. If any copyright issues are found in the articles on this website, please provide copyright questions, identification, proof of copyright, contact information, etc. and send an email to run@ebrun.com. We will communicate and handle it in a timely manner.

Translated by AI. Feedback: run@ebrun.com