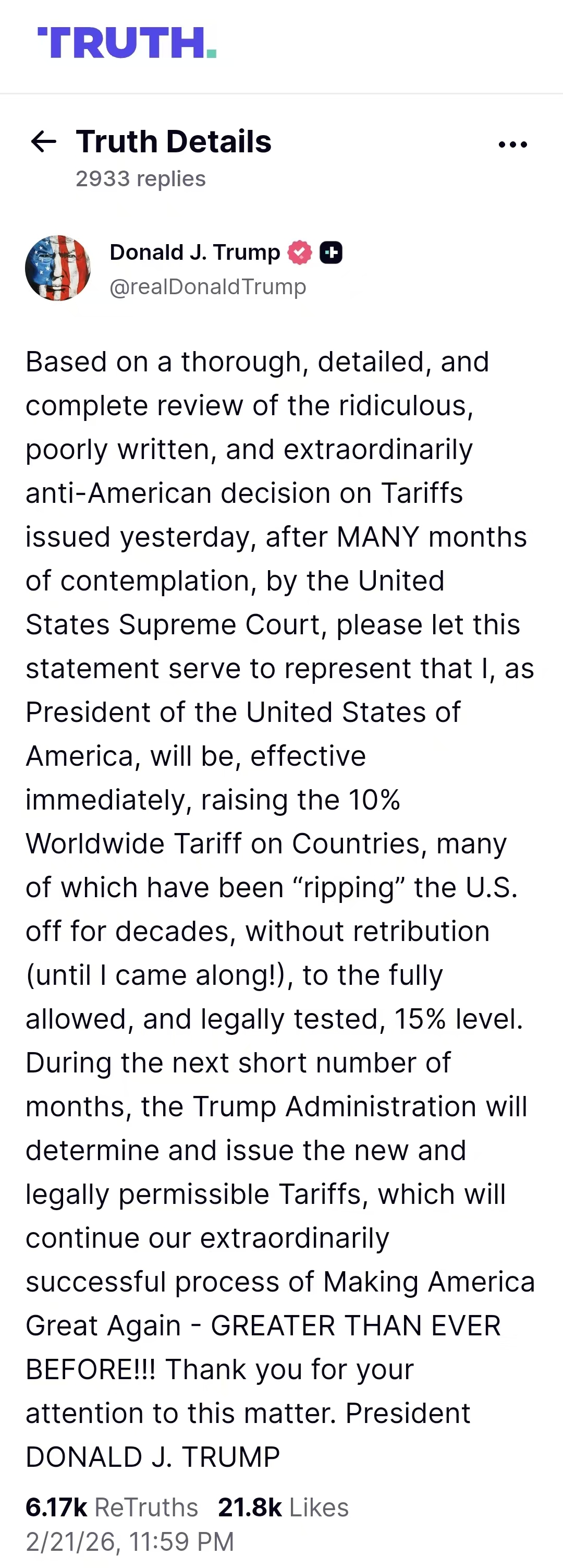

Trump Announces Global Tariff Increase to 15% to Counter Supreme Court Tax Reduction Ruling

[Ebrun Exclusive] February 22 - U.S. President Donald Trump announced on social media that he will raise the universal global tariff from 10% to 15%. This move comes just one day after the Supreme Court ruled that most of the tariffs he previously imposed under the International Emergency Economic Powers Act (IEEPA) were unlawful.

On the social platform Truth Social, he stated: "This decision was made after months of careful consideration. Please consider this statement as formal notice: I, as President of the United States, effective immediately, will increase the current 10% universal global tariff applied to various nations – many of whom have been 'exploiting' the United States for decades without any retaliation (until I came along!) – to a fully permissible and legally tested level of 15%."

He further added: "Over the coming months, the Trump administration will identify and announce new, legally permissible tariff measures, which will continue our extremely successful 'Make America Great Again' process – greater than ever before!"

This is reportedly Trump's second tariff increase action following the Supreme Court's ruling that he lacked the authority to unilaterally impose high tariffs under IEEPA – within hours of the February 21 ruling being announced, he quickly declared a 10% uniform import tariff on all countries worldwide.

The legal provision Trump invoked this time is Section 122 of the Trade Act of 1974.

This is a trade law tool independent of IEEPA, originally intended as an emergency measure to address serious U.S. balance of payments problems.

This law grants the President three key authorities: the ability to impose tariffs of up to 15% on imported goods, the ability to take trade measures such as quantitative restrictions, but these can only last a maximum of 150 days. Beyond 150 days, Congressional approval is required for continued implementation.

It is particularly noteworthy that Section 122 has never been actually used historically and lacks judicial precedent. Furthermore, this clause does not require the usual industry investigations, providing procedural convenience for the President to swiftly implement global tariffs. Trump is utilizing these characteristics to temporarily bypass the legal basis just invalidated by the Supreme Court.

Analysts point out that despite the 150-day time limit, the President could theoretically allow the "current tariff" to expire and then promptly declare another "balance of payments emergency," initiating a new round of temporary increases – creating a loop for cyclical tariff hikes.

Beyond "Section 122," Trump has various other policy tools at his disposal to maintain a high-tariff environment.

For example, "Section 301 investigations." This provision of the Trade Act of 1974 allows the U.S. Trade Representative to investigate whether a country engages in unfair trade practices and impose tariffs following the investigation. Trump used this authority during his first term to levy tariffs on Chinese imports, many of which remain in effect today. Theoretically, the administration could investigate a series of countries one by one and re-impose tariffs after each investigation concludes.

Another example is Section 232 of the Trade Expansion Act of 1962, which allows for restrictions on imports of products or from industries that threaten national security. If a Department of Commerce investigation confirms a threat exists, the President can impose tariffs or other trade restrictions. The Trump administration previously used this clause to levy tariffs on steel and aluminum products from numerous countries, such as the EU, Japan, South Korea, Brazil, Canada, and Mexico.

Furthermore, Section 338 of the Tariff Act of 1930 stipulates that the U.S. government can impose tariffs on goods from countries that "discriminate against U.S. commercial activities." The statute explicitly grants the government this power. Additionally, various anti-dumping / countervailing duty (AD/CVD) investigations are also considered temporary countermeasures that can be utilized.

These laws are independent and can be used to impose tariffs or restrictions on different countries, industries, products, or justifications separately. Even if one law is invalidated by the courts (like IEEPA), the President can still pursue tariff policies through other legal avenues – especially considering the lengthy process involved in any single Supreme Court ruling. This significantly increases Trump's room for maneuver using executive leverage to counter the Supreme Court.

Reviewing the event's origin, Trump's unusually aggressive measures stem from the Supreme Court's clear rejection on February 20, by a 6-3 majority, of the so-called "Trump tariffs."

The opinion stated that IEEPA does not grant the President the power to "impose comprehensive tariffs": while it allows the President to freeze assets and restrict transactions during a national emergency, the text does not explicitly authorize imposing broad-based import tariffs – the court held that the "power to lay tariffs" constitutionally belongs to Congress, therefore the President "exceeded statutory authorization."

The majority opinion noted that a universal global tariff involves "major economic and political questions" requiring explicit Congressional authorization; executive power cannot expand into the realm of taxation using "emergency powers" as a rationale, and the structural design of tariffs should be determined by the legislative branch.

Regarding refunds, while the Supreme Court's ruling did not directly order the federal government to automatically refund collected tariff payments, subsequent legal and fiscal impacts are rapidly emerging.

Under the U.S. administrative law framework, if a tariff measure is deemed to exceed statutory authority, the collection actions lack legal basis, and importers can seek refunds of paid duties plus interest through individual or class-action lawsuits. However, the scope of refunds, applicable timeframe, and potential retroactivity will depend on lower court enforcement procedures and specific arrangements by the Treasury Department.

Ebrun will continue tracking this development. To learn more related information, please scan the QR code to follow the author's WeChat.

[Copyright Notice] Ebrun advocates respecting and protecting intellectual property rights. Without permission, no one is allowed to copy, reproduce, or use the content of this website in any other way. If any copyright issues are found in the articles on this website, please provide copyright questions, identification, proof of copyright, contact information, etc. and send an email to run@ebrun.com. We will communicate and handle it in a timely manner.

Translated by AI. Feedback: run@ebrun.com